The term ‘bankruptcy’ can have a very doomsday connotation; the peak negative to financial troubles. It is also common to fear that it will be a lifelong black mark on your credit. While it will have an effect on your credit in the short and possibly long term, the bankruptcy period can finish earlier than you think. Although the bankruptcy term automatically ends in three years and one day from the date the Statement of Affairs is lodged, there are ways to cut it short.

First, the benefits of ending bankruptcy early

This is a valid consideration as the options below typically involve contributing funds to the estate over and above what you could be expected to contribute if the bankruptcy ran its full course. However, there are great reasons to work toward finalising your bankruptcy early. They include:

-

Income will no longer be assessed by the Trustee

-

You are no longer required to pay income contributions if assessed to be earning above the income threshold

-

Some professions have restrictions for undischarged bankrupts. By being discharged from bankruptcy sooner, you can re-enter the workforce

-

You can be a company director again

-

You can travel internationally without having to request written permission from your Trustee

-

You can obtain finance and credit sooner

-

The annulment effectively wipes the bankruptcy from the record as if it never happened.

So, how do you get there?

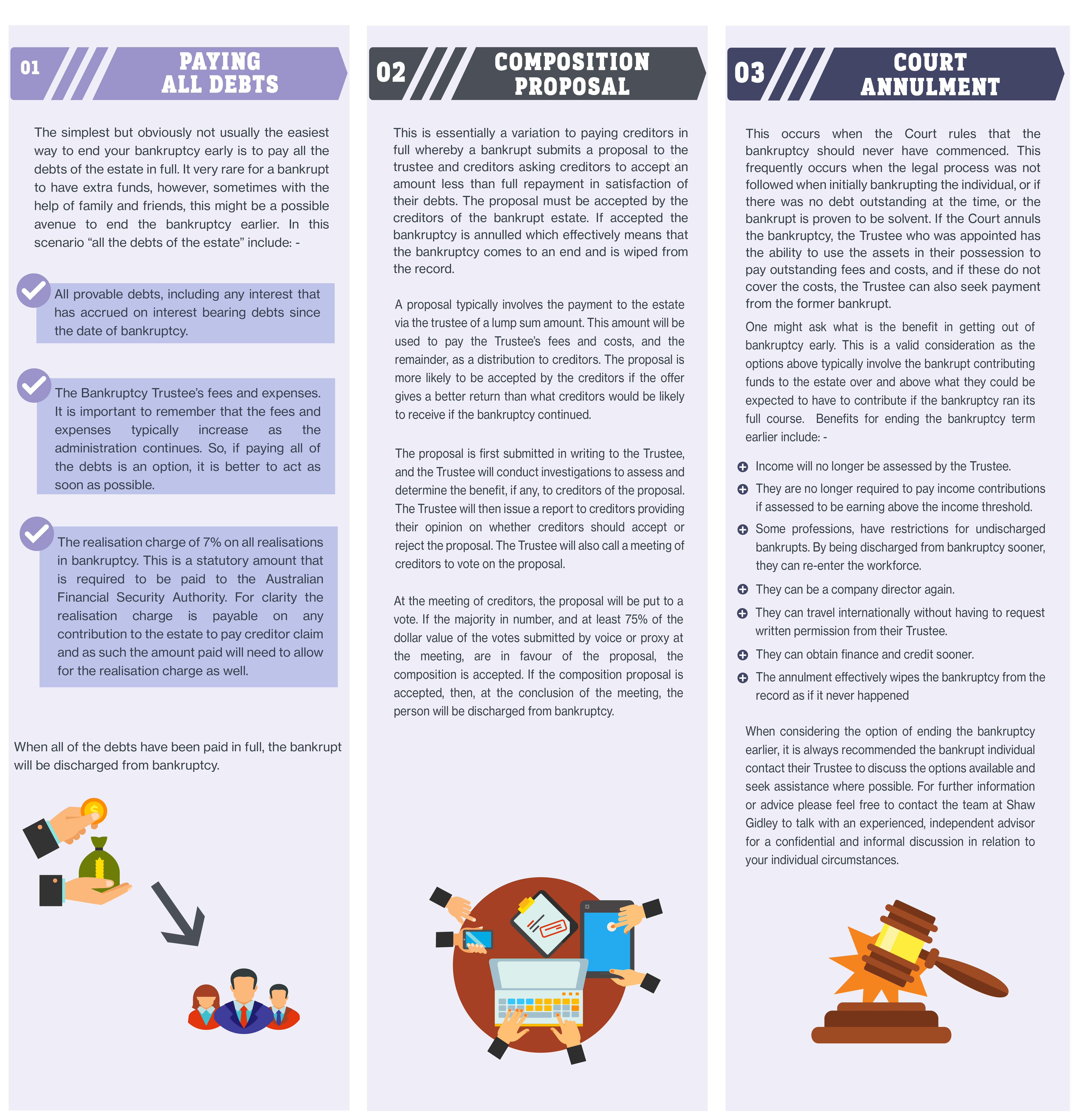

Paying all debts

While a seemingly simple and obvious solution, paying all debts of the estate in full is certainly not the easiest way to end your bankruptcy. If you’ve declared bankruptcy, it is very unlikely that you will have extra funds on hand. However, sometimes with the help of family and friends this might be a possible avenue to end your bankruptcy earlier. In this scenario, all the debts of the estate include:

-

All provable debts, including any interest accrued on interest bearing debts since the date of bankruptcy

-

The Bankruptcy Trustee’s fees and expenses typically increase as the administration continues. So, if paying all the debts is an option, it is better to act as soon as possible

-

The realisation charge of 7% on all realisations in bankruptcy is a statutory amount that is required to be paid to the Australian Financial Security Authority. For clarity, the realisation charge is payable on any contribution to the estate to pay creditors’ claim and, as such, the amount paid will need to allow for the realisation charge as well.

When all of the debts have been paid in full, you will be discharged from bankruptcy.

Composition proposal

This is essentially a variation to paying creditors in full. Here, you submit a proposal to the Trustee and creditors asking creditors to accept an amount less than full repayment in satisfaction of their debts. The proposal must be accepted by the creditors of the bankrupt estate. If accepted, the bankruptcy is annulled, effectively meaning that the bankruptcy comes to an end and is wiped from the record.

A proposal typically involves the payment to the estate via the Trustee of a lump sum amount. This amount will be used to pay the Trustee’s fees and costs (and the remainder) as a distribution to creditors. The proposal is more likely to be accepted by the creditors if the offer gives a better return than what creditors would be likely to receive if the bankruptcy continued.

The proposal is first submitted in writing to the Trustee, and the Trustee will conduct investigations to assess and determine the benefit, if any, to creditors of the proposal. The Trustee will then issue a report to creditors providing their opinion on whether creditors should accept or reject the proposal.

At the meeting of creditors, the proposal will be put to a vote. If the majority in number (and at least 75% of dollar value of the votes submitted by voice or proxy at the meeting) are in favour of the proposal, the composition is accepted. Then, at the conclusion of the meeting, you will be discharged from bankruptcy.

Court annulment

This occurs when the Court rules that the bankruptcy should never have commenced. This frequently occurs when the legal process was not followed initially, if there was no debt outstanding at the time, or the bankruptcy is proven to be solvent. If the Court annuls the bankruptcy, the Trustee who was appointed has the ability to use the assets in their possession to pay outstanding fees and costs. If these do not cover the costs, the Trustee can also seek payment from you.

When considering the option of ending the bankruptcy earlier, it is always recommended that you contact your Trustee to discuss the options available and seek assistance where possible.

Shaw Gidley are experts in restructuring, turnaround and insolvency and provide free initial advice on these matters. Please contact our offices on (02) 4908 4444 or (02) 6580 0400.

Want to keep this information on hand? Download the PDF for your reference.